What’s the Difference Between a HELOC and a Cash-Out Refinance? The Quiet Choice That Can Make or Break Your Plan for Wealth

If your home has equity, you may have heard the mantra: “Pull the equity out while money’s cheap.” While these are familiar words, they can ultimately destroy balance sheets far more often than most people acknowledge.

Because, quite literally, the manner in which you tap into the equity is just as important as the reasons you have for tapping into the equity. The two basic tools, as we noted, are quite different from one another.

When properly deployed, they put you in a position of leverage and flexibility. When misused, they set your financial clock back and keep you stuck for another decade.

Let’s put things into perspective.

The Core Difference (One Quick Sentence)

– Access to equity is available in a flexible way without using the main mortgage.

– A cash-out refinance replaces your old loan with an even larger, brand new, and shiny loan.

That contrast alone should give you pause.

What a HELOC Is (And When It Fits)

Home Equity Line of Credit is simply a credit line backed by your home, and the best way to think of it is this:

– First mortgage remains in place

– You borrow just what is needed

– You only pay interest on what you use

– You can pay it down and reuse it

HELOCs thrive in:

– You want short-term liquidity

– You’re spending capital on renovations, bridge capital, or opportunistic investment

– You want to keep your existing low rate

– You value flexibility over certainty

The risk:

– Most HELOCs are variable rate loans

– Payments can move

– Discipline matters, this is not free money

Therefore, for financially secure homeowners/investors, the HELOC is an instrument, not an enabler.

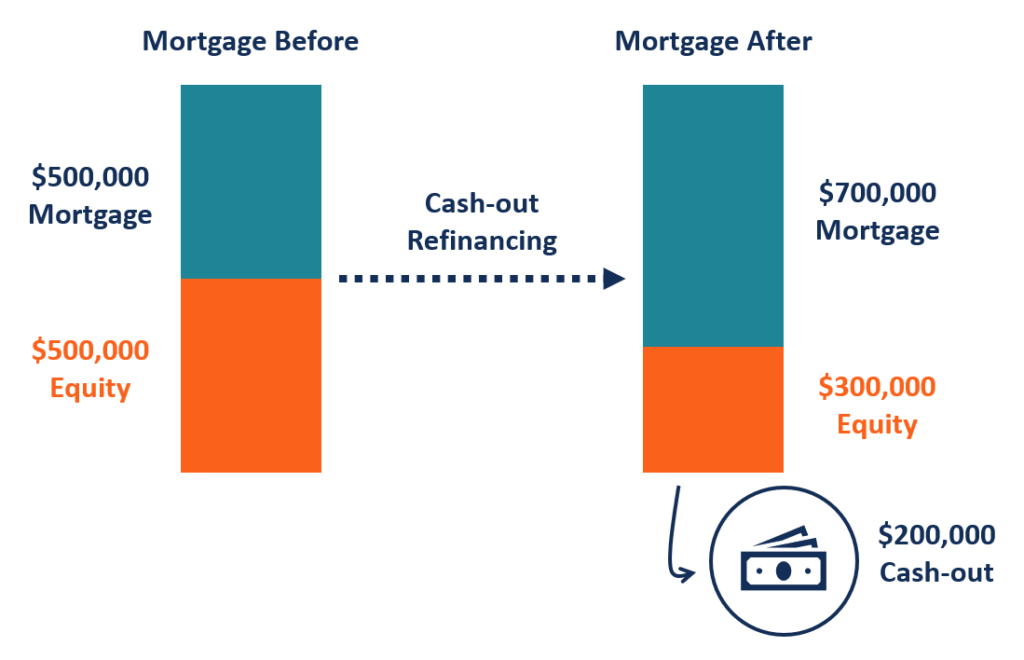

What a Cash-Out Refinance Really Does

A cash out refinance will pay off your existing mortgage and change it for a higher loan.

Sounds simple. But here’s the part most people miss:

You’re not “pulling cash.” You’re restarting debt.

What actually happens:

– Your loan balance increases

– Your amortization clock is usually reset (to 30 years)

– Yang keseluruhan minat hidup biasanya akan bert

– You no longer have protection from your old rate

The thing is that even when people state “no out-of-pocket,” that charge is included. It’s just built into the loan.

Cash-out refinances can be viable if:

– You’re wiping out toxic debt at much higher rates

– You crave long-term, fixed certainty

– You’re shooting for stability, not speed

But cutting one simply because the rates have gone down? Well, that’s where people get burned.

The Biggest Mistake Homeowners Make

They pose the wrong question.

Most people ask themselves:

“How much can I pull out?”

The better question, however, would be

“What does this decision cost me over time?”

Since a reduced monthly figure is not synonymous with financial success.

What really matters:

– Break-even Timeline

– Total Interest Paid

– Loss of the remaining loan term

– Future Flexibility

This is where, again, most guidance becomes unhelpfully vague.

Why This Matters More in California

In California, equity decisions are never made in a vacuum, as property taxes, property title, and ownership structure can create a simple refinance into an expensive blunder if the order is incorrect. Once triggered, several factors are difficult to reverse.

The Right Framework to Decide Before choosing between HELOC vs. cash-out, ensure that you can say yes to at least one of the following: – Does this improve short and long term outcomes? – Am I maintaining the lower fixed rate when ever possible? – Do I need permanent debt or just temporary access? – Do I know the real cost, and not just the price? If not, slow down. Good decisions age well; bad decisions exacerbate quickly. Final Thought Equity is power—as long as you control it. HELOCs lean toward flexibility and discipline. Cash-out refinance tends to lean toward certainty and structure. Neither is better than the other. One can be less forgiving. And once you reset that clock, you can’t stop it.